Will Visa Stock Split Again 2018

Sezeryadigar/E+ via Getty Images

Are you lot worried about this overvalued stock market place? Later on the epic run the market has been on over the concluding few years, or even decade, a lot of investors are.

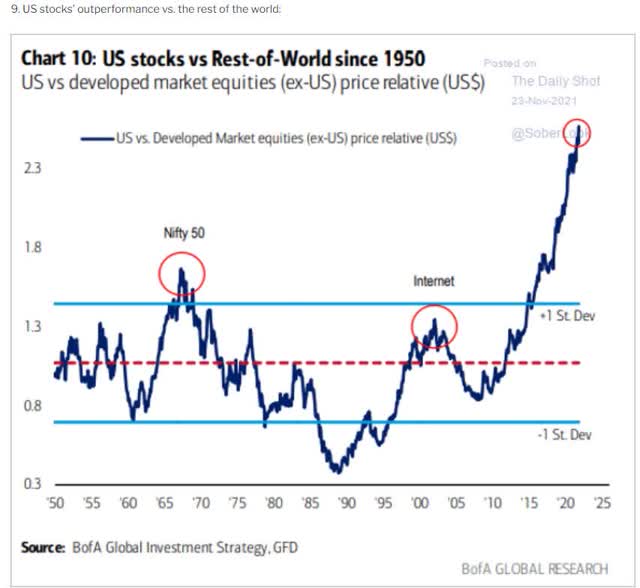

Are stocks overvalued? Absolutely, particularly compared to foreign peers.

Compared to the residue of the globe, Usa stocks are the nearly overvalued in the last 71 years.

Compared to the residue of the globe, Usa stocks are the nearly overvalued in the last 71 years.

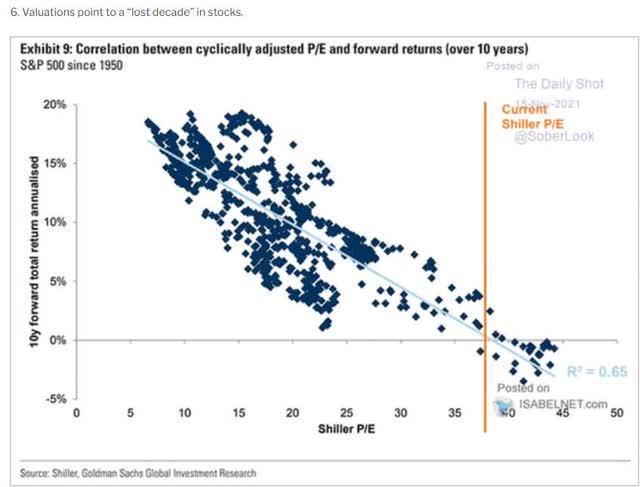

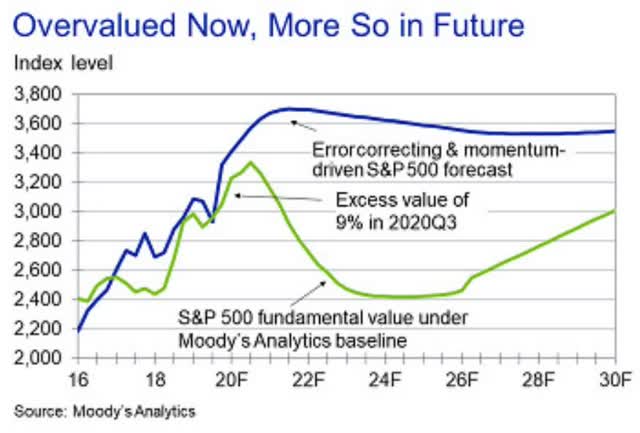

Goldman thinks that the S&P is potentially headed for a lost decade. Moody'due south agrees.

Goldman thinks that the S&P is potentially headed for a lost decade. Moody'due south agrees.

The good news for investors is that FactSet and JPMorgan don't expect a lost decade for the market. They estimate the market place to be about 30% historically overvalued and thus likely to evangelize weak returns over the next v years.

The good news for investors is that FactSet and JPMorgan don't expect a lost decade for the market. They estimate the market place to be about 30% historically overvalued and thus likely to evangelize weak returns over the next v years.

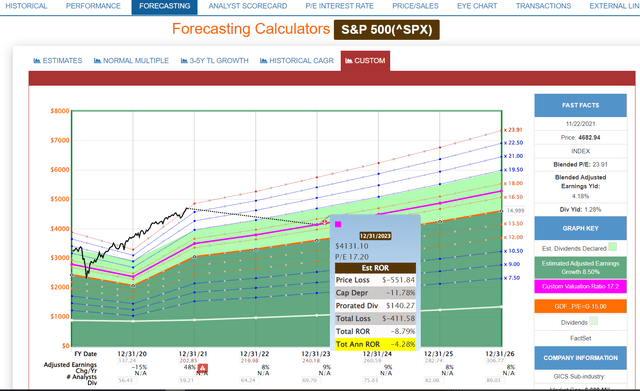

S&P 500 2023 Consensus Total Return Potential

(Source: FAST Graphs, FactSet Inquiry)

(Source: FAST Graphs, FactSet Inquiry)

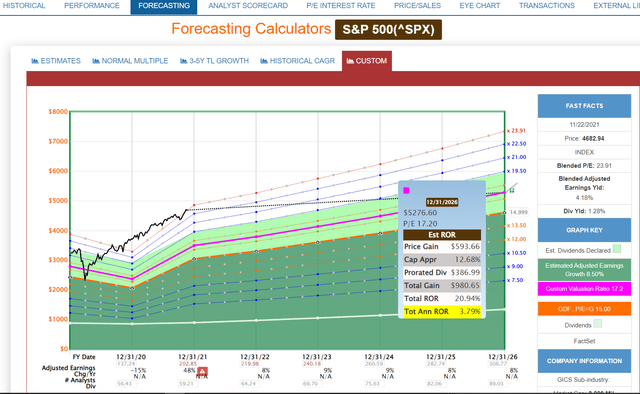

S&P 500 2026 Consensus Total Return Potential

(Source: FAST Graphs, FactSet Enquiry)

(Source: FAST Graphs, FactSet Enquiry)

Analysts await the S&P 500 to deliver about 21% total returns over the adjacent five years.

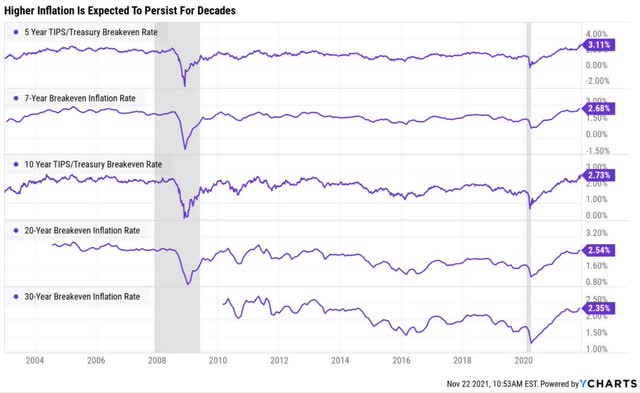

Inflation And Risk-Adapted Expected Returns

Year Upside Potential Past End of That Year Consensus CAGR Return Potential By End of That Twelvemonth Probability-Weighted Return (Annualized) 2021 -24.86% -87.08% -65.31% -68.31% 2022 -17.08% -fifteen.17% -11.38% -xiv.38% 2023 -8.00% -3.82% -2.87% -5.87% 2024 1.40% 0.44% 0.33% -2.67% 2025 11.60% 2.69% 2.02% -0.98% 2026 22.67% 4.06% two.89% -0.25%

(Source: DK S&P 500 Valuation And Total Return Tool) updated weekly

Adapted for inflation, the chance-expected returns of the S&P 500 are near zero for the next five years.

So not a lost decade, simply potentially a lost 3 to five years, depending on whether y'all gene in inflation.

So what's the answer? Sell everything and hide in cash?

Over the long-term cash is 100% guaranteed to lose value.

Over the long-term cash is 100% guaranteed to lose value.

- over the next 30 years, the bail marketplace expects cash to deliver -51% returns

How nigh foreign companies which are likely to see strong mean reversion outperformance at some bespeak?

(Source: Morningstar)

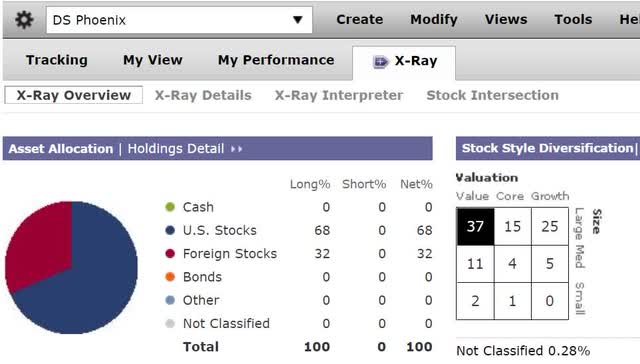

My retirement portfolio is 32% foreign companies, mostly deep value names that are poised to soar in the coming years.

Only what if yous are a US-focused dividend growth investor wanting to safely buy the globe's highest quality companies. Not merely to protect yourself from inflation today, but to aid you retire rich tomorrow and stay rich in retirement no matter what the market or economic system does in the future?

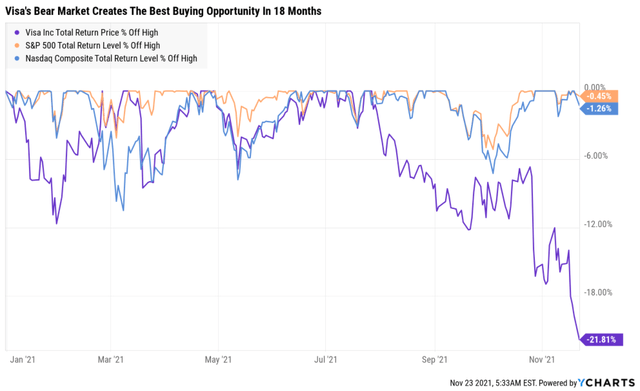

In this carmine hot market place Visa (NYSE:V), which is equally close to a perfect quality hyper-growth dividend baddest, is down 22%.

Is the thesis broken? Is Visa a "falling knife" that investors should avert similar the plague?

Analyst Median 12-Calendar month Toll Target Morningstar Fair Value Approximate Discount To Price Target (Not A Fair Value Gauge) Discount To Fair Value Upside To Price Target (Non Including Dividend) Upside To Fair Value (Not Including Dividend) 12-Calendar month Median Full Render Price (Including Dividend) Fair Value + 12-Calendar month Dividend Discount To Total Price Target (Not A Fair Value Estimate) Discount To Fair Value + 12-Month Dividend Upside To Price Target ( Including Dividend) Upside To Fair Value + Dividend

$274.38 $217 (DCF model = 31.1 PE) 28.72% 9.87% xl.29% 10.95% $275.88 $218.50 29.eleven% ten.49% 41.06% eleven.72%

Analysts expect Visa to more than than quadruple the market's returns in the next 21 months.

Forward Overvaluation Forecast (12 Months From At present)

12-Calendar month Forward S&P Bottom-Upwards Consensus 5142.95 Forward PE Forecast (12 Months From Now) 12-Calendar month Consensus Market Return Potential 9.8% 21.63 28.vii%

(Source: DK S&P 500 Valuation & Total Return Tool)

We don't really care nearly 12-month cost targets, which never accept any basis in our recommendations. What we care about are the fundamentals that ultimately bulldoze 91% of long-term returns.

Total Returns Explained Past Fundamentals/Valuations

Time Frame (Years) 1 Day 0.02% one calendar month 0.4% three month 1.25% 6 months 2.5% one 5% ii xvi% 3 25% 4 33% 5 41% half dozen 49% 7 57% 8 66% ix 74% 10 82% xi+ 90% to 91%

(Sources: DK South&P 500 Valuation And Total Return Potential Tool, JPMorgan, Banking company of America, Princeton, RIA)

- over 12 months luck is 20X as powerful as fundamentals

- over xi+ years fundamentals are 11X as powerful as luck

Well then my friends, let me tell you 5 reasons why you should potentially buy Visa (V) now before everyone else does.

In fact, these five reasons make Visa a classic Buffett-way "Wonderful visitor at a fair cost" and could be just what you demand to help your portfolio have a smashing 2022 and beyond.

Reason One: This Behave Market Is A Potentially Wonderful Buying Opportunity

Kickoff, permit's address why Visa has fallen 22% in a thing of weeks as the market makes record high after tape high.

Amazon announced it will stop accepting Visa credit cards issued in the U.K. starting in tardily January 2022, citing its conventionalities that fees on these cards are too high. Consumers volition notwithstanding be immune to employ U.Grand.-issued Visa debit cards. Merchants and the networks have argued for many years over interchange fees, and information technology is typically large merchants that lead the charge. At this point, this looks like only another skirmish in this long-running battle, although refusing to have specific cards is an extreme step. Following Brexit, the networks were no longer constrained by European Marriage regulations on U.K. cantankerous-border transactions and raised their fees. The networks typically collect a very large premium for cross-border transactions relative to domestic transactions, only intra-Europe cross-edge transactions are priced similarly to domestic transactions. With both networks raising fees, information technology is not obvious why Visa has been singled out, although nosotros believe Amazon may have a stronger relationship with Mastercard in the U.K or considered declining cards from both networks to be a step too far. At this betoken, the conclusion of this issue remains uncertain, although the companies have until January 2022 to work out a solution. If they don't, we don't believe the loss of volume would be fabric relative to Visa's overall business and believe this proclamation would merely be pregnant if it prompted other retailers to follow suit. Just nosotros consider this unlikely. We will maintain our $217 fair value gauge and wide moat rating for Visa." - Morningstar (accent added)

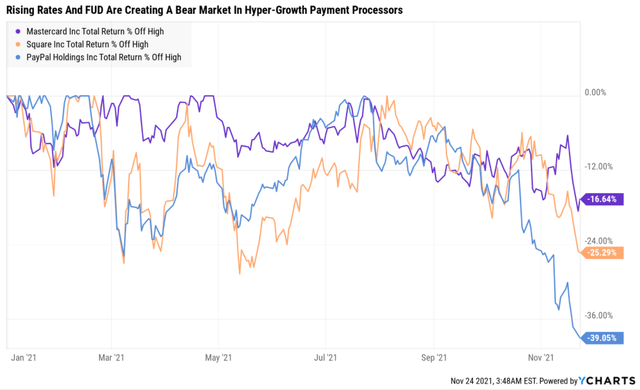

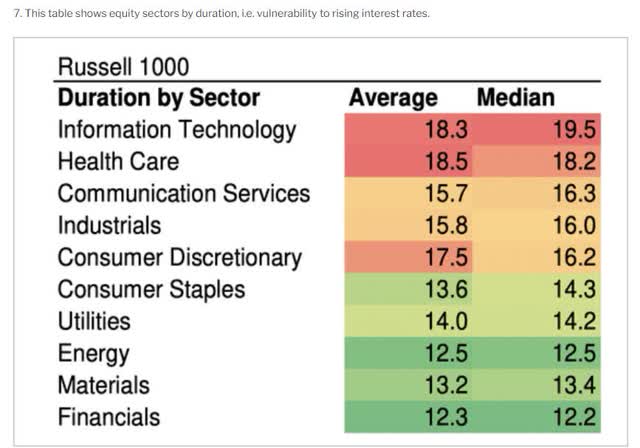

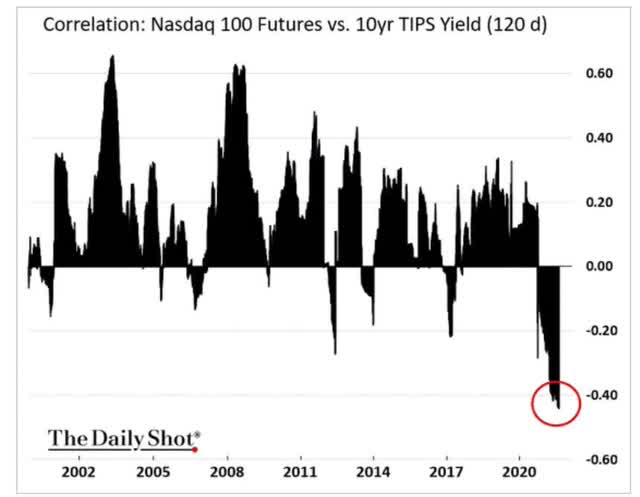

Payment processors in general, ranging from Mastercard (MA), Paypal (PYPL), and Square (SQ) have all been suffering due to rising interest rates and concerns about potential manufacture disruption.

In the risk section, I'll explain why these companies are adapting to the rise of disruptive threats like Blockchain and Buy-Now-Pay Later, but another reason for their sharp sell-off is rising involvement rates.

(Source: Daily Shot)

(Source: Daily Shot)

Faster growing companies tend to exist the most rate-sensitive and that's never been more true at today's loftier valuations for growth stocks.

In other words, high valuations combined with ascent rates and now something scary happening in the headlines is the likely reason why payment processors like Visa take sold off so sharply.

In other words, high valuations combined with ascent rates and now something scary happening in the headlines is the likely reason why payment processors like Visa take sold off so sharply.

2025 Consensus

Metric 2020 Growth 2021 Growth Consensus 2022 Growth Consensus 2023 Growth Consensus 2024 Consensus Sales -5% x% 17% fourteen% 12% 10% Dividends twenty% 7% 17% (Official) 8% 19% 24% EPS -7% 17% 20% 19% 16% 29% Owner Earnings (Buffett smoothed out FCF) -18% NA NA NA NA NA Operating Cash Flow -17% 24% 16% eight% 29% 25% Free Cash Menses -18% 52% fifteen% sixteen% NA NA EBITDA -v% -4% 20% 16% 14% xiv% EBIT (operating income) -6% -three% 19% sixteen% 16% xiii%

(Source: FAST Graphs, FactSet Research)

Analysts, rating agencies, and the bail market all hold, that Visa'southward long-term thesis remains intact.

This is Non a "falling knife" value trap, whose fundamentals are falling as fast or faster than the stock price.

In fact, let me testify you just how not broken Visa's thesis actually is.

Reason Two: Visa Is One Of The World'southward Best Companies

The Dividend King'due south overall quality scores are based on a 220 indicate model that includes:

-

dividend rubber

-

balance canvas forcefulness

-

credit ratings

-

credit default bandy medium-term defalcation chance data

-

short and long-term defalcation risk

-

accounting and corporate fraud take chances

-

profitability and concern model

-

growth consensus estimates

-

cost of capital

-

long-term hazard-direction scores from MSCI, Morningstar, FactSet, South&P, Reuters'/Refinitiv and Just Capital

-

direction quality

-

dividend friendly corporate civilisation/income dependability

-

long-term total returns (a Ben Graham sign of quality)

-

analyst consensus long-term return potential

It actually includes over 1,000 metrics if you count everything factored in by 12 rating agencies we utilize to appraise fundamental risk.

-

credit and hazard management ratings brand upwardly 38% of the DK safe and quality model

-

dividend/residue sheet/adventure ratings make up 79% of the DK safe and quality model

How practice nosotros know that our safety and quality model works well?

During the two worst recessions in 75 years, our prophylactic model predicted 87% of blue-chip dividend cuts during the ultimate baptism by fire for any dividend safety model.

How does Visa score on one of the world's most comprehensive and accurate safety models?

Dividend Safety

Judge Dividend Cut Risk In Pandemic Level Recession

Rating Dividend Kings Condom Score (133 Point Safety Model) Approximate Dividend Cut Risk (Boilerplate Recession) 1 - unsafe 0% to 20% over 4% 16+% two- beneath average 21% to 40% over 2% viii% to 16% 3 - average 41% to threescore% two% 4% to 8% four - safe 61% to 80% 1% 2% to 4% 5- very condom 81% to 100% 0.five% one% to 2% V 94% 0.fifty% 1.30%

Long-Term Dependability

Company DK Long-Term Dependability Score Interpretation Points Non-Dependable Companies 18% or below Poor Dependability i Depression Dependability Companies 19% to 57% Below-Average Dependability two South&P 500/Industry Average 58% (58% to 67% range) Average Dependability 3 Above-Average 68% to 77% Very Dependable 4 Very Good 78% or higher Exceptional Dependability 5 V 78% Infrequent Dependability 5

Overall Quality

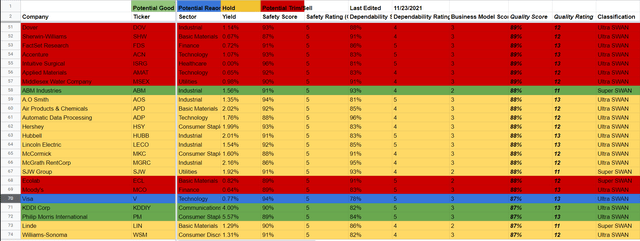

V Concluding Score Rating Prophylactic 93% 5/five very prophylactic Business Model 90% three/iii wide moat Dependability 78% 5/5 exceptional Total 87% 13/13 Ultra SWAN

Visa: 69th Highest Quality Primary Listing Company (Out of 507) = 86th Percentile

(Source: DK Safety & Quality Tool) updated daily, sorted past overall quality

(Source: DK Safety & Quality Tool) updated daily, sorted past overall quality

The DK 500 Principal List includes the earth's highest quality companies including:

-

All dividend champions

-

All dividend aristocrats

-

All dividend kings

-

All global aristocrats (such every bit BTI, ENB, and NVS)

-

All 13/13 Ultra Swans (as close to perfect quality equally exists on Wall Street)

- 42 of the world's all-time growth stocks (on its way to 50)

Visa's 87% quality score means its similar in quality to such blue-fries as

- Linde (LIN) - dividend aristocrat

- Philip Morris International (PM) - dividend king

- Ecolab (ECL) - dividend aristocrat

- McCormick (MKC) - dividend aristocrat

- Automatic Data Processing (ADP) - dividend blueblood

- Air Products & Chemicals (APD) - dividend aristocrat

- A.O Smith (AOS) - dividend aristocrat

- Dover (DOV) -dividend king

Fifty-fifty among the world'south highest quality companies, Visa is higher quality than 86% of them.

What makes Visa so safe and dependable?

Visa Credit Ratings

Rating Bureau Credit Rating 30-Twelvemonth Default/Bankruptcy Risk Chance of Losing 100% Of Your Investment 1 In S&P AA- stable 0.55% 181.8 Moody'south Aa3 (AA- equivalent) stable 0.55% 181.viii Consensus AA- stable 0.55% 181.8

(Sources: South&P, Moody'due south)

How most a 0.55% fundamental run a risk of losing all your money in the next xxx years?

Visa Leverage Consensus Forecast

Interest Coverage (8+ Condom)

Year Debt/EBITDA Net Debt/EBITDA (3.0 Or Less Prophylactic According To Credit Rating Agencies) 2020 1.62 0.27 27.32 2021 1.25 0.xv 31.21 2022 1.00 -0.05 37.50 2023 0.85 -0.19 44.31 2024 0.81 -0.52 59.49 Annualized Alter -15.86% NA 21.48%

(Source: FactSet Research)

How virtually a residue canvas that is expected to take more than cash than debt past 2022?

Visa Balance Canvass Consensus Forecast

Yr Total Debt (Millions) Cash Net Debt (Millions) Interest Toll (Millions) EBITDA (Millions) Operating Income (Millions) Interest Costs 2020 $24,070 $16,289 $4,029 $516 $xiv,864 $14,098 ii.fourteen% 2021 $20,977 $16,487 $two,465 $513 $16,780 $16,013 two.45% 2022 $19,890 $nineteen,199 -$ane,072 $512 $nineteen,872 $19,202 2.57% 2023 $xix,529 $twenty,147 -$4,311 $503 $22,948 $22,288 two.58% 2024 $xx,977 $41,044 -$13,401 $426 $25,845 $25,344 2.03% 2025 NA NA NA NA $28,316 $27,419 NA Annualized Growth -3.38% 25.99% NA -4.68% 13.76% 14.23% -1.34%

(Source: FactSet Inquiry)

How nigh double-digit cash flow growth and a cash position that'southward already $16.5 billion and growing at 26% per twelvemonth?

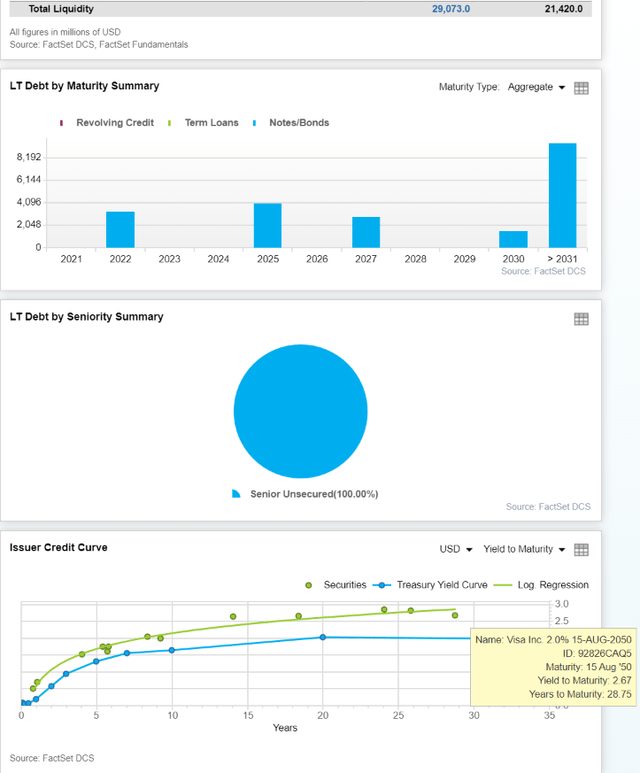

Visa Bond Profile

(Source: FactSet Research)

The smart money on Wall Street is and then confident in Visa's business organization it'southward willing to lend to it for 29 years at 2.7%.

Today Visa'due south borrowing costs are 2.39% and are expected to autumn to 2% inside a few years.

- adjusted for the bond market's long-term two.35% inflation expectations Visa is borrowing for free

- and investing that coin at a cash return on invested capital of 25%

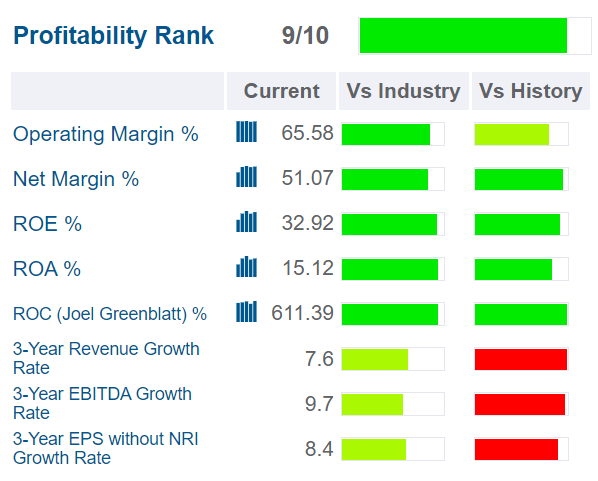

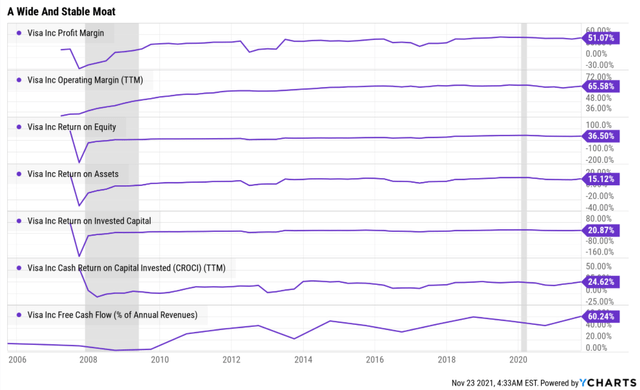

Speaking of profitability, that's Wall Street'south favorite proxy for quality and Visa's is merely astonishing.

Visa Profitability: Wall Street'south Favorite Quality Proxy

(Source: GuruFocus Premium)

Payment processing is a highly lucrative industry and Visa'southward profitability is historically in the top 10% of its peers.

Visa Abaft 12-Month Profitability Vs Peers

Metric Industry Percentile Major Credit Processors More Profitable Than V (Out Of 371) Operating Margin 87.06 48 Net Margin 84.76 57 Render On Equity 93.31 25 Return On Assets 94.90 NA Return On Uppercase 94.61 xx Average ninety.93 34

(Source: GuruFocus Premium)

In the last year it'southward in the top nine% of its peers.

Visa'southward free cash flow margins are in the tiptop 1% of all companies on globe.

Its net profit margins of over 50% are the stuff of legend.

Visa Margin Consensus Forecast

Return On Capital Forecast

Yr FCF Margin EBITDA Margin EBIT (Operating) Margin Net Margin Return On Uppercase Expansion 2020 46.3% 68.0% 64.v% 51.2% i.04 2021 threescore.two% 69.half-dozen% 66.4% 53.7% TTM ROC 611.39% 2022 56.viii% 70.3% 68.0% 53.iii% Latest ROC 652.60% 2023 56.4% 71.0% 68.9% 54.7% 2025 ROC 635.15% 2024 58.six% 71.4% seventy.1% 55.7% 2025 ROC 677.96% 2025 57.3% 71.three% 69.0% 54.8% Average 656.55% 2026 NA NA NA NA Manufacture Median 64.88% Annualized Growth four.34% 0.93% 1.35% 1.37% Visa/Peers 10.12 Vs Due south&P 50.50

(Source: FactSet Research)

Over the coming years, analysts expect Visa's profitability to rise even further, despite all the various risks its facing from industry disruptors.

And as far as render on capital goes, Joel Greenblatt's gilded standard proxy for quality and moatiness? Visa's ROC is over 600% and is expected to remain stable over time, at 10X college than its peers and 51X college than the S&P 500.

Joel Greenblatt delivered xl% annualized returns for 21 years at Gotham Majuscule focusing purely on quality and valuation. And according to one of the greatest investors in history, Visa is one of the highest quality companies on world.

Reason 3: Visa's Hyper-Growth Thesis Remains Firmly Intact

Visa was founded in 1958 in San Francisco and is the earth'southward largest credit card processing network.

Visa is the largest payment processor in the earth. In fiscal 2020, information technology processed almost $9 trillion in purchase transactions. Visa operates in over 200 countries and processes transactions in over 160 currencies. Its systems are capable of processing over 65,000 transactions per second...

Visa traces its roots dorsum to the issuance of the kickoff Bank of America cards in the belatedly 1950s. Every bit credit cards grew, partnerships betwixt credit card issuers became necessary, and Visa as a brand was formed in 1976. In the decades since, Visa has been one of the largest beneficiaries of the shift toward electronic payments. In fiscal 2020, the company processed about $9 trillion in purchase transactions. Visa has almost xvi,000 financial institution partners, iii.iv billion Visa cards in circulation, and over 50 million merchants accepting Visa.

According to the Nilson Study, Visa holds over l% market share (by buy volume) in the U.S., Europe, Latin America, and the Middle East/Africa. Visa also processes roughly twice equally many transactions as its closest competitor, Mastercard. Simply put, Visa'southward position in the world of electronic payments is unparalleled. We don't believe that building a new network with a comparable size and reach is realistic over any foreseeable time line, and view Visa'due south position inside the current global electronic payment infrastructure every bit essentially unassailable." - Morningstar (emphasis added)

Morningstar considers their moat "essentially unassailable". I wouldn't go that far but with over 50 one thousand thousand merchants on its network and $eleven.4 trillion in processing volumes in the last fiscal yr, it's a very wide moat company indeed.

(Source: FactSet Research)

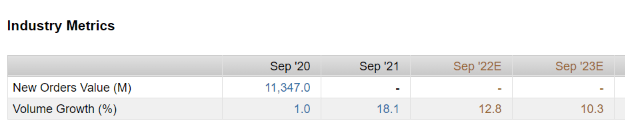

For context, FactSet'south $11.35 trillion in transactions in 2020 represents approximately 11% of global GDP.

(Source: earnings presentation)

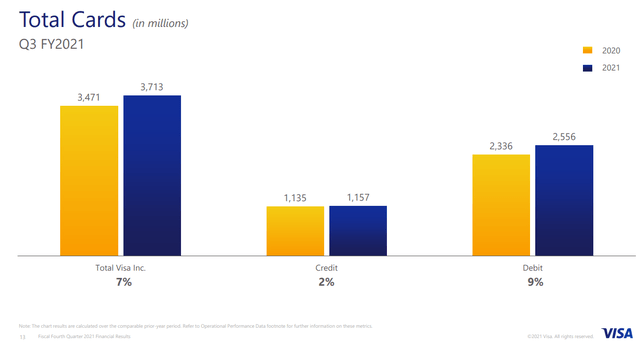

Visa is upward to iii.7 billion cards in global apportionment, growing at seven% in the past year. And with most 85% of all global transactions yet in cash, there is plenty of growth runway left for Visa.

How much?

Visa Medium-Term Consensus Forecast

Year Sales Gratis Greenbacks Flow EBITDA EBIT (Operating Income) Cyberspace Income 2020 $21,846 $ten,120 $14,864 $14,098 $11,193 2021 $24,105 $xiv,522 $16,780 $16,013 $12,933 2022 $28,258 $16,040 $19,872 $xix,202 $fifteen,069 2023 $32,337 $18,234 $22,948 $22,288 $17,687 2024 $36,173 $21,195 $25,845 $25,344 $20,144 2025 $39,731 $22,757 $28,316 $27,419 $21,790 Annualized Growth 2020-2025 12.71% 17.59% 13.76% 14.23% 14.25%

(Source: FactSet Research)

In just the next few years analysts expect Visa'southward costless cash flow to grow at almost 18% annually.

Its dividend is expected to grow by nearly sixteen% per year and EPS by 18%.

Visa Dividend Growth Consensus Forecast

Twelvemonth Dividend Consensus Earnings/share Consensus Payout Ratio Retained Earnings Buyback Potential Debt Repayment Potential 2021 $i.28 $v.91 21.vii% $10,107 2.43% 48.2% 2022 $1.44 $seven.03 xx.five% $12,203 two.93% 58.2% 2023 $1.55 $8.44 xviii.4% $fifteen,041 three.62% 75.vi% 2024 $one.85 $ix.82 18.8% $17,399 4.18% 89.i% 2025 $2.30 $xi.48 20.0% $20,040 iv.82% 95.5% Total 2021 Through 2025 $8.42 $42.68 nineteen.7% $74,789.58 17.98% 356.53% Annualized Charge per unit 15.78% 18.06% -1.93% 18.66% 18.66% 18.66%

(Source: FactSet Research)

- 60% or less is the safe payout ratio for this industry

- Visa historically runs 1/3 that

- 16% dividend growth but xviii% earnings growth resulting in a very safe dividend

- enough retained earnings to repay 357% of its debt or buyback 18% of its shares

How much do analysts expect Visa to spend on buybacks?

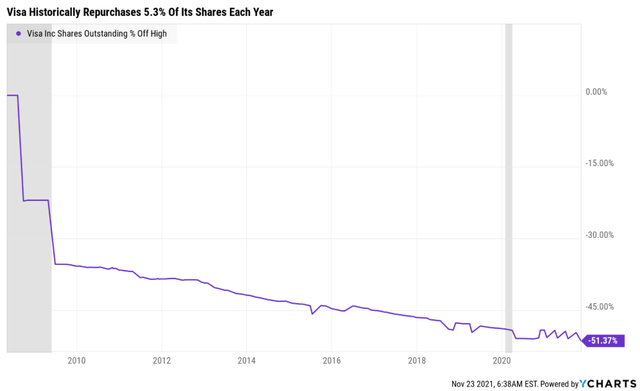

- $30.87 billion betwixt 2021 and 2023

- 7.iv% of shares over three years

- ii.4% of shares each yr

What near the long-term?

Visa Long-Term Growth Outlook

(Source: FactSet Research)

- 16.1% to 17.7% CAGR growth consensus range

- smoothing for outliers five% margin of error to the downside and 15% to the upside

- 15% to 21% CAGR historical margin-of-mistake adjusted growth consensus range

(Source: FAST Graphs, FactSet Enquiry)

Visa is expected to go on growing at the aforementioned charge per unit every bit the last decade. A rate that'southward approximately 2X equally fast equally the South&P 500's profits are expected to grow.

OK, so we accept one of the world'due south best companies, growing at nearly 17% according to analysts, even with the contempo Amazon news, and a 22% bear marketplace.

That means that Visa, for the kickoff time in nearly 18 months, is at present reasonably valued. In fact, it'due south a archetype Buffett-style "wonderful company at a fair price".

Reason Four: A Classic Buffett-Style "Wonderful Company At A Fair Price"

I don't speculate almost what a company is worth. I only let the market, over the long-term tell me what a blue-chips quality, risk profile, and growth prospects are worth.

(Source: FAST Graphs, FactSet Research)

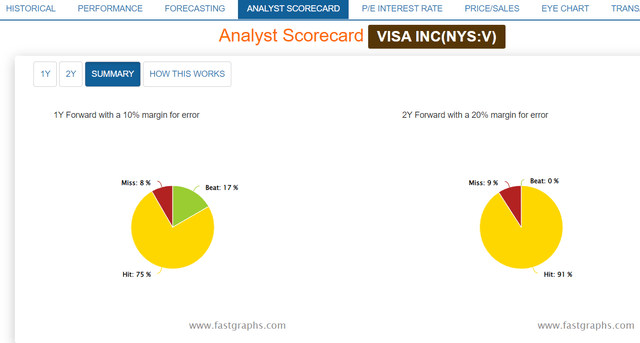

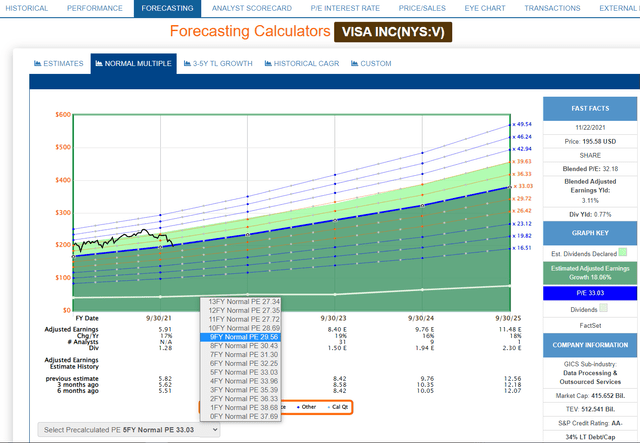

Since its IPO hundreds of millions of investors accept paid between 27.5X and 31.5X earnings for Visa.

- a 90% statistical probability that is range represents the visitor's intrinsic value

Disbelieve To Fair Value Current Forrad PE

Metric Historical Fair Value Multiples (10-Years) 2021 2022 2023 2024 2025 12-Calendar month Forward Fair Value 13-Year Median P/South 13.05 $147.47 $173.57 $198.36 $221.85 $244.04 5-Year Average Yield 0.63% NA $238.10 $246.03 $293.65 $365.08 13-Twelvemonth Median Yield 0.63% $238.x $238.ten $246.03 $293.65 $365.08 xiii-yr Average Yield 0.69% $217.39 $217.39 $224.64 $268.12 $333.33 Earnings 29.22 $172.67 $206.73 $246.01 $286.94 $335.45 Operating Cash Flow 31.46 $183.33 $213.20 $229.49 $347.63 $429.43 Gratis Greenbacks Menses 34.06 $226.15 NA $300.06 NA NA EBITDA 20.35 NA NA $178.87 $204.11 $233.62 EBIT (operating income) 21.33 $130.71 $155.85 $181.ten $209.89 $237.xix Average $179.95 $201.70 $222.28 $266.07 $315.79 $199.61 Electric current Price $195.58 -8.69% iii.03% 12.01% 26.49% 38.07% 2.02% Upside To Off-white Value -seven.99% 3.13% xiii.65% 36.04% 61.47% ii.06% 2021 PE 2022 PE 2022 Weighted EPS 12-Calendar month Forward EPS 12-Month Boilerplate Fair Value Frontward PE $5.91 $7.08 $6.40 $6.97 28.half dozen 28.one

Visa is trading at 28.1X forrad earnings, slightly beneath its average trimmed harmonic off-white value of 28.6X.

What does that actually mean?

12-Calendar month Forward Fair Value Upside To Off-white Value (Not Including Dividends)

Rating Margin Of Safety For 13/13 Ultra SWAN Quality Companies 2021 Cost 2022 Toll Potentially Reasonable Buy 0% $179.95 $201.70 $199.61 Potentially Expert Buy 5% $170.95 $191.61 $189.63 Potentially Strong Buy 15% $152.96 $171.44 $169.66 Potentially Very Strong Buy 25% $128.21 $151.27 $149.70 Potentially Ultra-Value Buy 35% $116.97 $131.10 $129.74 Currently $195.58 -8.69% 3.03% ii.02% -7.99% 3.xiii% 2.06%

That for anyone comfortable with its run a risk contour, Visa is a potentially reasonable purchase. And here's why.

Reason Five: Market Bang-up Total Return Potential In Both The Short And Long-Term

Here's what investors ownership Visa today tin can reasonably expect.

- 5-twelvemonth consensus render potential range: 14% to 20% CAGR

Visa 2023 Consensus Full Return Potential

(Source: FAST Graphs, FactSet Research)

(Source: FAST Graphs, FactSet Research)

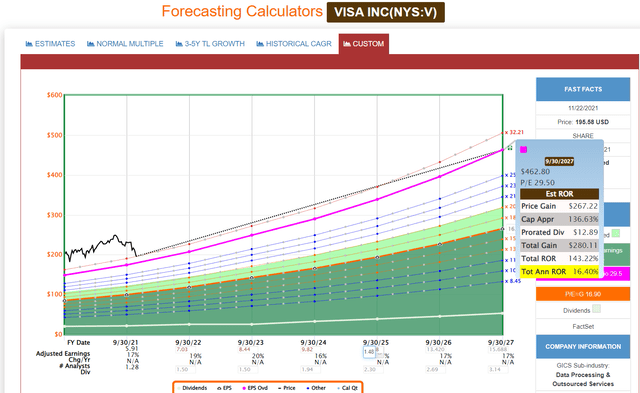

Visa 2026 Consensus Full Return Potential

(Source: FAST Graphs, FactSet Research)

(Source: FAST Graphs, FactSet Research)

Over the next five years, analysts expect 21% returns from the S&P 500 and potentially 140% from Visa, 7X improve consensus return potential.

Visa Investment Decision Score

First-class

Ticker five DK Quality Rating 13 87% Investment Form A Sector Technology Prophylactic v 94% Investment Score 95% Industry IT Services Dependability 5 78% 5-Year Dividend Return 5.88% Sub-Industry Data Processing & Outsourced Services Business Model 3 Today's 5+ Yr Risk-Adjusted Expected Return 12.23% Ultra SWAN, Phoenix, Hyper-Growth, Strong ESG Goal Scores Scale Estimation Valuation 3 Reasonable Purchase v's ii.02% discount to fair value earns it a 3-of-4 score for valuation timeliness Preservation of Capital 7 Excellent v's credit rating of AA- implies a 0.55% hazard of bankruptcy risk, and earns it a 7-of-7 score for Preservation of Capital letter Render of Capital N/A Due north/A N/A Return on Capital x Exceptional v'south 12.23% vs. the Southward&P'south 2.89% 5-twelvemonth adventure-adjusted expected return (RAER) earns it a 10-of-10 Return on Capital score Total Score 20 Max score of 21 South&P's Score Investment Score 95% 73/100 = C(Market Average) Investment Letter Grade A

(Source: DK Automated Investment Conclusion Tool)

For those comfy with its risk contour, Visa is one of the all-time hyper-growth bluish-fries you tin buy in today'due south 30% overvalued market.

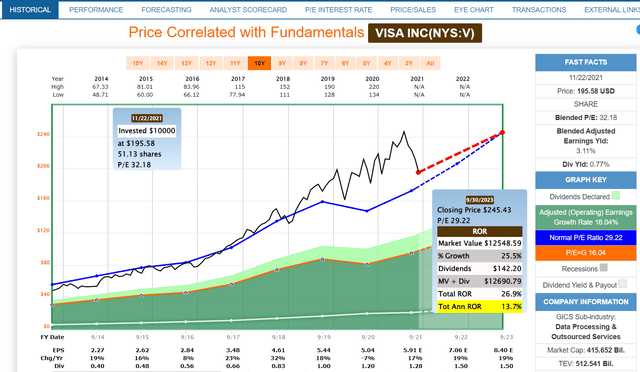

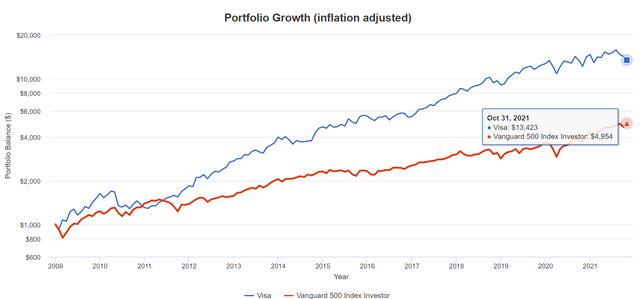

Visa Total Returns Since 2009

(Source: Portfolio Visualizer)

(Source: Portfolio Visualizer)

- yield in 2009: 0.8% (same equally today)

- the yield on cost 2021: ten.7%

- income growth (including dividend reinvestment): 24.1% CAGR

Visa S&P 500 Vs Aristocrats Inflation-Adapted Long-Term Return Forecast: $ane,000 Investment

- the bail market is pricing in two.35% inflation for the side by side 30 years

- 3.1% for the next 5 years

Fourth dimension Frame (Years) 7.55% CAGR Inflation-Adjusted Due south&P Consensus 8.85% Inflation-Adjusted Aristocrat Consensus fourteen.55% CAGR Visa consensus Difference Betwixt Visa And Southward&P 5 $ane,438.97 $1,528.07 $ane,972.31 $533.34 10 $two,070.64 $2,334.99 $iii,890.01 $1,819.37 fifteen $2,979.59 $three,568.01 $7,672.31 $4,692.73 20 $four,287.54 $five,452.16 $15,132.xix $ten,844.65 25 $vi,169.65 $8,331.26 $29,845.forty $23,675.75 30 $8,877.94 $12,730.72 $58,864.41 $49,986.47 35 $12,775.xi $19,453.38 $116,098.95 $103,323.84 40 $18,383.01 $29,726.06 $228,983.26 $210,600.26 45 $26,452.62 $45,423.39 $451,626.28 $425,173.67 50 $38,064.55 $69,409.94 $890,747.63 $852,683.08

Fourth dimension Frame (Years) Ratio Aristocrats/S&P Ratio Visa Vs S&P 500 5 i.06 1.37 ten one.13 1.88 15 1.twenty 2.57 20 1.27 three.53 25 1.35 iv.84 30 1.43 6.63 35 1.52 9.09 forty one.62 12.46 45 one.72 17.07 50 1.82 23.40

Combining Visa with loftier-yield Ultra SWANs like MMP can deliver safe income today, and a rich retirement tomorrow.

- 3 Ways 8.9% Yielding Magellan Midstream Can Help You Retire Rich

Visitor Ticker Yield Growth Consensus Long-Term Consensus Full Return Potential Weighting Weighted Yield Weighted Growth Weighted Total Return Potential Conservative Adventure-Adapted Expected Return Altria MO 8.eighteen% five.3% 13.v% 0.00% 0.0% 0.0% 0.0% ix.44% Amazon AMZN 0.00% 23.ii% 23.2% 0.00% 0.0% 0.0% 0.0% xvi.24% British American BTI viii.62% 4.2% 12.8% 0.00% 0.0% 0.0% 0.0% viii.97% Magellan Midstream Partners (K-i Taxation Class) MMP 8.78% 5.4% xiv.2% fifty.00% 4.four% 2.vii% vii.1% 9.92% Meta Platforms FB 0.00% 17.6% 17.6% 0.00% 0.0% 0.0% 0.0% 12.32% Enbridge (CA Visitor, 15% Tax Withholding) ENB 6.83% 8.iv% 15.ii% 0.00% 0.0% 0.0% 0.0% 10.66% Philip Morris International PM v.57% 11.8% 17.4% 0.00% 0.0% 0.0% 0.0% 12.16% Alphabet GOOG 0.00% 21.9% 21.9% 0.00% 0.0% 0.0% 0.0% 15.33% Visa 5 0.77% sixteen.v% 16.9% 50.00% 0.four% viii.iii% 8.v% 11.83% Mastercard MA 0.55% 22.1% 22.1% 0.00% 0.0% 0.0% 0.0% 15.47% Starbucks SBUX 1.76% 11.0% 11.0% 0.00% 0.0% 0.0% 0.0% vii.lxx% Docusign DOCU 0.00% l.0% 50.0% 0.00% 0.0% 0.0% 0.0% 35.00% Paypal PYPL 0.00% 21.6% 21.vi% 0.00% 0.0% 0.0% 0.0% xv.12% Activision Blizzard ATVI 0.76% 12.iv% xiii.two% 0.00% 0.0% 0.0% 0.0% 9.21% Dividend Aristocrats NOBL ii.30% 8.nine% 11.2% 0.00% 0.0% 0.0% 0.0% seven.84% Nasdaq QQQ 0.68% 10.9% xi.6% 0.00% 0.0% 0.0% 0.0% 8.11% S&P 500 VOO i.xl% 8.5% 9.9% 0.00% 0.0% 0.0% 0.0% half dozen.93% threescore/40 BAGPX 1.90% 5.ane% 7.0% 0.00% 0.0% 0.0% 0.0% 4.90% US Bonds SCHZ 1.30% 0.0% 1.3% 0.00% 0.0% 0.0% 0.0% 0.91% Cash VGSH 0.30% 0.0% 0.three% 0.00% 0.0% 0.0% 0.0% 0.21% Bitcoin BTC 0.00% 60.0% 35.0% 0.00% 0.0% 0.0% 0.0% 24.50% Ether ETH 0.00% eighty.0% fifty.0% 0.00% 0.0% 0.0% 0.0% 35.00% BlockFi USDC 9.00% 0.0% 9.0% 0.00% 0.0% 0.0% 0.0% vi.30% Total 49.69% 278.0% 325.0% 100.00% iv.8% xi.0% xv.5% x.88%

(Source: DK Portfolio Construction Tool)

Visa + MMP offers a very safety iv.8% yield, 11.0% overall growth, 15.8% consensus render potential, and xi.0% risk-adjusted expected returns.

Long-Term Inflation And Risk-Adjusted Expected Returns

Investment Strategy Yield LT Consensus Growth LT Consensus Total Return Potential Long-Term Risk-Adjusted Expected Render Safe Midstream five.8% 6.two% 12.0% 8.4% six.ane% Visa + MMP 4.eight% 11.0% 15.8% 11.0% viii.7% Safe Midstream + Growth iii.3% eight.5% 11.8% 8.3% 5.9% REITs 3.0% 7.0% 9.ix% 6.9% 4.half dozen% High-Yield ii.vii% 11.0% 13.seven% 9.6% 7.2% Dividend Aristocrats 2.3% 8.9% 11.2% 7.9% v.5% Value 2.1% 12.i% 14.ii% ten.0% seven.half dozen% threescore/40 Retirement Portfolio one.ix% 5.1% 7.0% 4.9% ii.6% REITs + Growth i.eight% viii.9% 10.6% 7.4% five.1% High-Yield + Growth i.7% 11.0% 12.vii% 8.nine% half-dozen.v% 10-Twelvemonth United states of america Treasury 1.61% 0.0% 1.vi% 1.6% -0.7% S&P 500 1.iv% eight.five% 9.9% 6.9% 4.6% Nasdaq (Growth) 0.7% 11.0% 11.7% 8.2% v.8% Chinese Tech 0.3% fourteen.0% 14.3% ten.0% 7.7%

(Sources: Morningstar, FactSet Research)

Higher safe yield than loftier-yield ETFs? Yes.

Faster growth than the Nasdaq? That's what analysts think.

Better risk-adjusted returns than virtually any other investment strategy on Wall Street? You bet.

This is the Zen Phoenix strategy in activity.

- Zen Phoenix: always buy growth with yield and yield with growth

- always at fair value or better

- and always focusing on safety and quality first and sound risk direction ever

- balance in all things that thing (safety, quality, risk management, yield, growth, and value)

But earlier you go too excited virtually Visa just recollect that even the earth's highest quality Ultra SWANs yet have a risk profile you must be comfy with before investing.

Gamble Profile: Why Visa Isn't Right For Everyone

At that place are no risk-gratuitous companies and no visitor is right for anybody. Y'all have to exist comfy with the fundamental risk contour.

Visa Risk Profile Summary

Visa'southward acquirement is tied to the corporeality and volume of consumer purchases, which creates macroeconomic sensitivity. Both Visa and Mastercard have paid substantial fines historically related to the oligopolistic nature of the manufacture, and legal and regulatory risk is intrinsic to the business organisation model, given merchants' desires to lower fees. While Visa'south and Mastercard's positions in the electric current electronic payment industry are largely set, it continues to evolve in ways that could reduce their book or profitability. Some governments have shown a preference for local payment networks, which could freeze Visa out of sure markets and impede the value it drives from its global network.

We see the company'southward largest ESG run a risk every bit data security. Any company involved in processing payments has potential exposure to breaches in its systems." - Morningstar(emphasis added)

Visa's Risk Profile Includes

- economic cyclicality hazard (especially cross border transactions, which are the well-nigh assisting and thus impacted by the pandemic)

- regulatory chance (anti-trust concerns)

- disruption risk (370 major peers, Block-chain theoretically volition allow 2X the capacity at 5% the cost...or less, Buy-now-pay later is another major disruption risk)

- M&A execution take chances (regulators might try to block K&A in the hereafter, plus potentially overpaying for fast-growing fintechs)

- talent retentivity risk (tightest chore market in over 50 years)

- data security risk: hackers and ransomware

- currency risk (54% of sales outside the US)

Buy At present Pay Afterward or BNPL is a newer instance. Merely nosotros call back we'll have a similar outcome. While installments are fast-growing, there only a fraction of the total manufacture's payment volume is estimated to exist about 100 to 150 billion. Merely nosotros are bringing scale to disruptors. We have a two-pronged strategy where nosotros provide a network solution as well as solutions for our BNPL, Fintech partners...

We have nigh 60 crypto platform partners with the capability to consequence Visa credentials, and in that location -- we're already capturing over 3.5 billion of payment volume in FY21....

As a reminder, the boost we saw in Q3 was primarily from cryptocurrency purchases." - CEO, Q3 conference call

Visa has invested in and partnered with BNPL and crypto fintechs to ensure information technology gets a piece of whatever future pie they create.

(Source: JPMorgan Asset Management)

(Source: JPMorgan Asset Management)

How practice we quantify, monitor, and track such a complex hazard contour? Past doing what big institutions do.

Material Fiscal ESG Risk Analysis: How Large Institutions Measure Total Risk

- 4 Things You Demand To Know To Profit From ESG Investing

- What Investors Need To Know About Company Long-Term Risk Management (Video)

Here is a special report that outlines the nearly important aspects of understanding long-term ESG financial risks for your investments.

- ESG is Non "political or personal ethics based investing"

- information technology'southward full long-term risk direction analysis

ESG is but normal risk by another name." Simon MacMahon, head of ESG and corporate governance research, Sustainalytics" - Morningstar

ESG factors are taken into consideration, alongside all other credit factors, when we consider they are relevant to and have or may take a fabric influence on creditworthiness." - S&P

ESG is a measure of risk, not of ethics, political correctness, or personal opinion.

S&P, Fitch, Moody'due south, DBRS (Canadian rating agency), AMBest (insurance rating agency), R&I Credit Rating (Japanese rating agency), and the Nippon Credit Rating Agency have been using ESG models in their credit ratings for decades.

- credit and take a chance management ratings brand up 38% of the DK safe and quality model

- dividend/balance sheet/risk ratings make up 79% of the DK safety and quality model

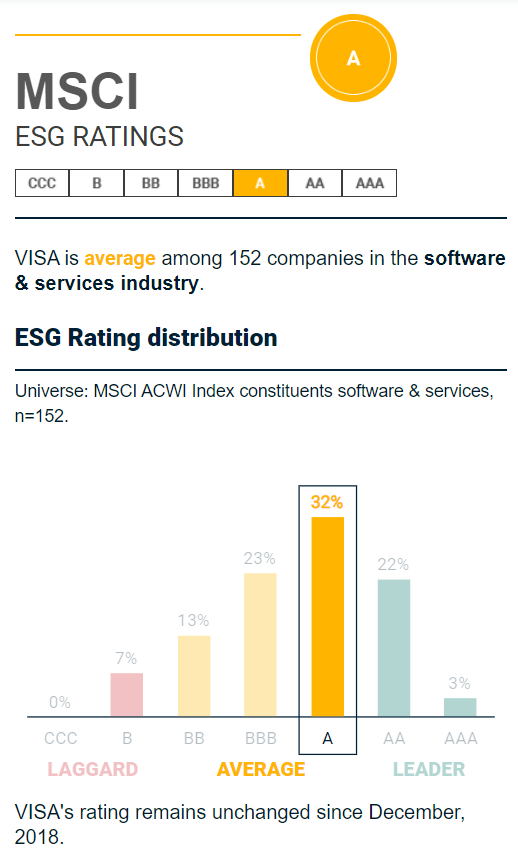

Dividend Aristocrats: 67th Industry Percentile On Risk Management (Above-Average, Medium Chance)

(Source: Morningstar)

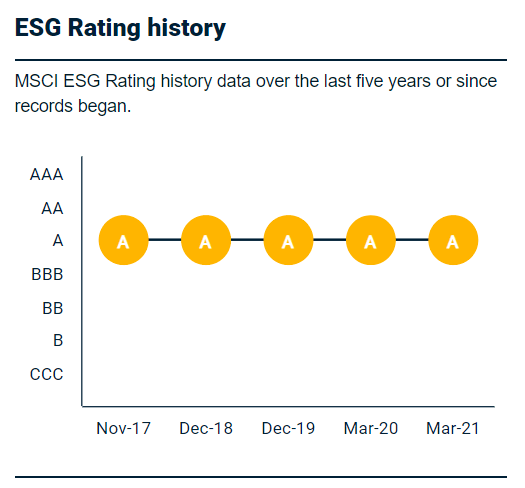

Visa Long-Term Risk Direction Consensus

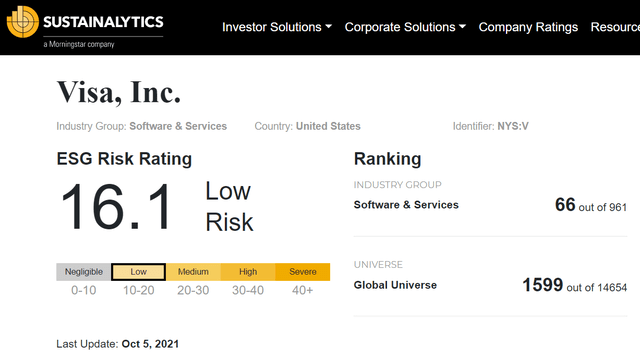

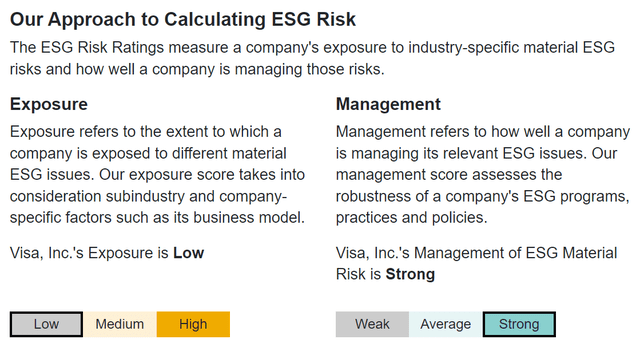

Rating Bureau Classification A, higher up-average 16.1/100 Depression-Hazard

Rating Agency Industry Percentile MSCI 37 Metric Model 75.0% Morningstar/Sustainalytics 20 Metric Model 93.i% Reuters'/Refinitiv 500+ Metric Model 79.1% Good South&P ane,000+ Metric Model 63.0% Higher up-Average Simply Capital 19 Metric Model 85.00% Excellent Consensus 79.1% Adept FactSet Qualitative Assessment Below-Boilerplate Stable Tendency

(Sources: Morningstar, Reuters', S&P, Only Capital, FactSet Research)

(Source: MSCI)

(Source: MSCI)

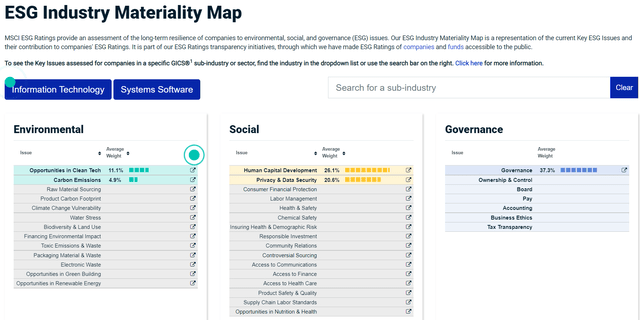

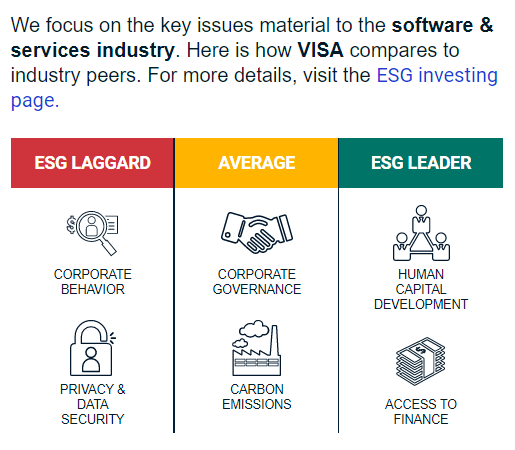

According to MSCI'due south 185 industry experts, 5 major risk factors are of import to consider for this industry.

- environmental is just 16% of MSCI's weighting

- data security is more than important to Visa's risk profile than environmental concerns

- governance is #1 weighting for virtually ESG gamble models and that's true for MSCI too, at 37%

(Source: MSCI)

- MSCI is incorrect

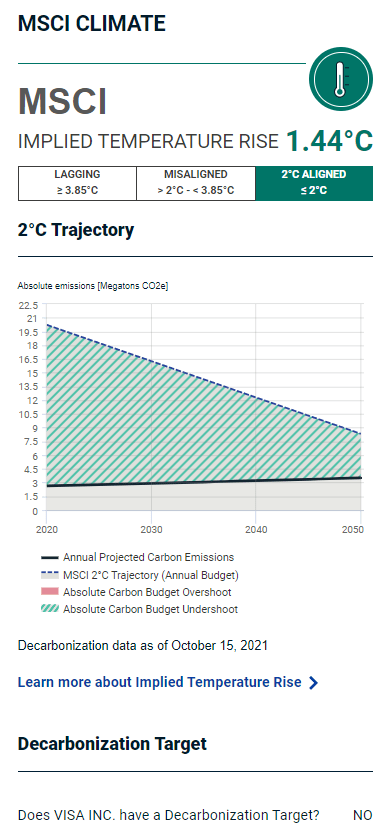

- Visa has a target of becoming carbon-neutral past 2040

Implied Temperature Ascension compares the current and projected greenhouse gas emissions of nearly 10,000 publicly listed companiesii beyond all emissions scopes (based on the visitor'south track record and stated reduction targets) with their share of the remaining global carbon upkeep for keeping warming this century well below 2 degrees Celsius (2°C).3 A visitor projected to emit carbon beneath budget can be said to "undershoot" the budget a company projected to exceed the budget "overshoots" it.

- telescopic 1 = a visitor's ain emissions

- scope ii = supply concatenation

- score three = end users

(Source: MSCI)

- scary headlines about regulations or lawsuits? ESG hazard scores already measure out information technology

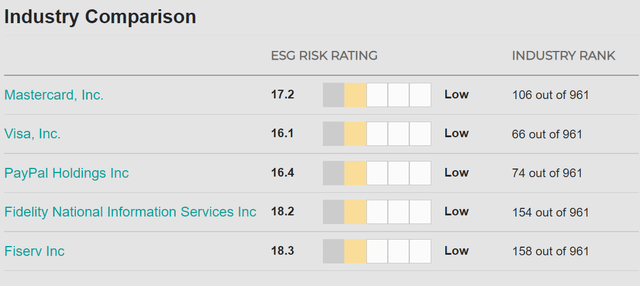

(Source: Morningstar) - 20 metric model

- 93rd industry percentile

- 89th percentile among most xv,000 globally rated companies

(Source: Reuters'/Refinitiv) - over 500 metric model

(Source: Reuters'/Refinitiv) - over 500 metric model

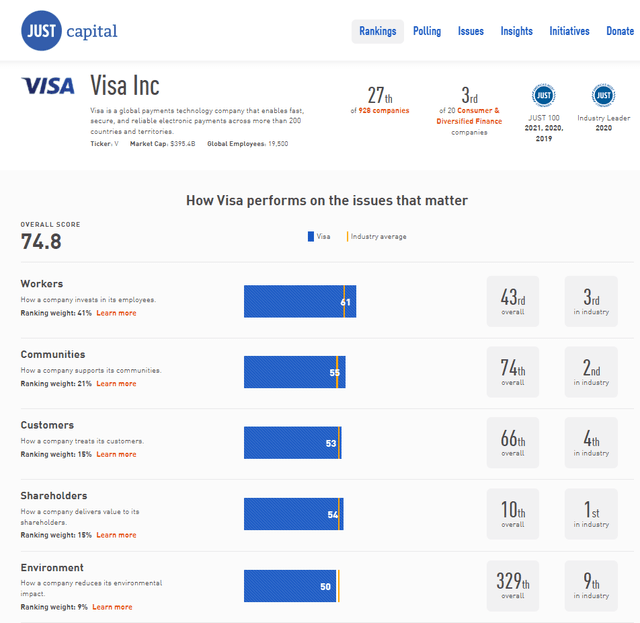

Reuters considers Visa's risk management to be in the 79th industry percentile with an 85/100 full general chance management (CSR strategy) which is splendid.

(Source: Southward&P)

Southward&P's take chances management model, which is included in all its credit ratings, uses publically available information for over 1,000 primal metrics, ranging from talent memory/employee skill investments to supply chain management to occupational health and safety.

- But Capital'south rating is based on a survey of 110,000 Americans about which of xix risk factors they consider near important for companies

- then using publically bachelor data, they rank 928 of America's largest companies

- 75 total sub metrics are used to calculate these scores

(Source: Only Capital)

(Source: Only Capital)

- 85th industry percentile

- #1 in the manufacture in 2020

- Top 100 amongst American companies in 2019, 2020 and 2021

- 97 percentile among United states of america companies

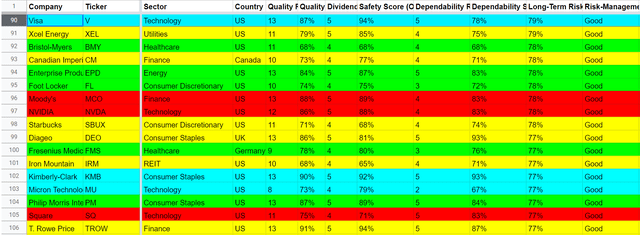

Visa'due south Long-Term Risk Management Is The 82nd All-time In The Master Listing (82nd Percentile)

(Source: DK Principal List) - 7 non-rated companies hateful Visa is in 82nd identify

(Source: DK Principal List) - 7 non-rated companies hateful Visa is in 82nd identify

Visa's risk-management consensus is in the peak 18% of the world'southward highest quality companies and similar to that of such other companies every bit

- T. Rowe Toll (TROW) - dividend aristocrat

- Philip Morris International (PM) - dividend male monarch

- Kimberly-Clark (KMB) - dividend blueblood

- Diageo (DEO)

- NVIDIA (NVDA)

- Enterprise Products Partners (uses One thousand-one taxation grade) (EPD)

- Canadian Imperial Banking concern of Commerce (CM)

- Bristol-Myers (BMY)

The bottom line is that all companies accept risks, and Visa is skilful at managing theirs.

How We Monitor Visa'south Risk Profile

- 37 analysts

- 2 credit rating agencies

- 7 total risk rating agencies

- 44 experts who collectively know this business concern improve than anyone other than direction

- and the bond market, the "smart money" on Wall Street

Rest assured, that if Visa'southward thesis weakens, strengthens, or breaks entirely, we'll know well-nigh information technology so volition our members.

What Would Intermission/Weaken The Thesis On Visa

- Dividend safety falls to xl% or less (unsafe)

- growth consensus falls to less than ix.2% for a twelvemonth - would be removed from Phoenix list (and get a "personal hold" for me)

- growth consensus stays less than 9.two% or less for one year, I'd consider selling l%

- growth consensus stays less than nine.two% or less for two years I'd consider selling the entire position

- Visa's role in any portfolio is to generate x+% total returns, which requires at least ix.2% growth

When the facts change, I change my mind. What practise yous practice sir?" - John Maynard Keynes

There are no sacred cows at Dividend Kings. Wherever the fundamentals pb we always follow. That'southward the essence of disciplined financial science, the math retiring rich and staying rich in retirement.

Bottom Line: This Carry Market place In Visa Is A Potentially Wonderful Long-Term Buying Opportunity

Just because the market place is thirty% overvalued and potentially set for a very disappointing few years for stocks, doesn't mean that in that location aren't notwithstanding amazing blueish-chip opportunities for smart investors to take advantage of.

Visa'due south recent bear market has finally brought it back to fair value, making it a archetype Buffett-style "wonderful company at a fair cost".

One that could evangelize nearly 18% annualized long-term returns in the years and decades ahead.

And if y'all combine it with high-yield bluish-chips like MMP then yous can enjoy well-nigh 5% very safe yield today, while waiting for potentially 16% long-term returns in the future.

Am I saying that analysts are correct and Visa is fix to soar 41% in the next year? Absolutely not, that's non at all justified by its fundamentals.

What I am saying is that Visa's consensus fundamentals indicate a 27% potential full return in the next two years, and 143% in the next five years.

That's not merely 7X more than than the Due south&P 500 is expected to potentially deliver but could be just what your diversified and prudently take a chance-managed portfolio needs to beat inflation today, retire rich tomorrow, and stay rich in retirement.

Are you tired of cursing the Fed for record low-interest rates and record-high stock prices?

Are you sick of worrying about every marketplace gyration and trying to brusk-term merchandise your way to prosperity?

Then information technology's time to stop praying for luck on Wall Street, and start making your ain.

Luck is what happens when preparation meets opportunity." - Roman philosopher Seneca the younger

Buying Visa earlier it fell 22% and was about xx% overvalued, was not reasonable or prudent.

Buying it now at off-white value? That'southward sound disciplined financial scientific discipline and could prove to exist one of the best long-term dividend growth investments yous e'er brand.

Source: https://seekingalpha.com/article/4472219-5-reasons-to-buy-visa-before-everyone-else-does

0 Response to "Will Visa Stock Split Again 2018"

Post a Comment